Understanding BEAT in Plain English

The Base Erosion and Anti-Abuse Tax (BEAT) is a special surtax meant to keep very large U.S.-based multinationals from stripping earnings out of the country. It was created in 2017 and comes into effect whenever a company’s U.S. income is whittled down by big payments to foreign affiliates for:

- Loan interest

- Royalties on intellectual property

- Management or service fees

These are called “base erosion payments” because they shrink the company’s U.S. tax base. BEAT is a backstop: if your ordinary U.S. tax bill (after credits) falls below a minimum, BEAT tops it up.

Who Is Affected?

BEAT rules target large companies who have made significant base erosion payments:

- Large companies: Average over $500 million in gross receipts (3-year look-back)

- Meaningful base erosion: At least 3% of total deductions (2% if a bank or broker) paid to related foreign parties

Meet both criteria and you must compute two tax bills:

1. Regular corporate tax (21%), reduced by credits

2. BEAT tax – rebuilds the base, applies a flat BEAT rate, and ignores most credits

Simply put, you always pay the regular tax. If BEAT is bigger, you pay the difference—a “top-up.”

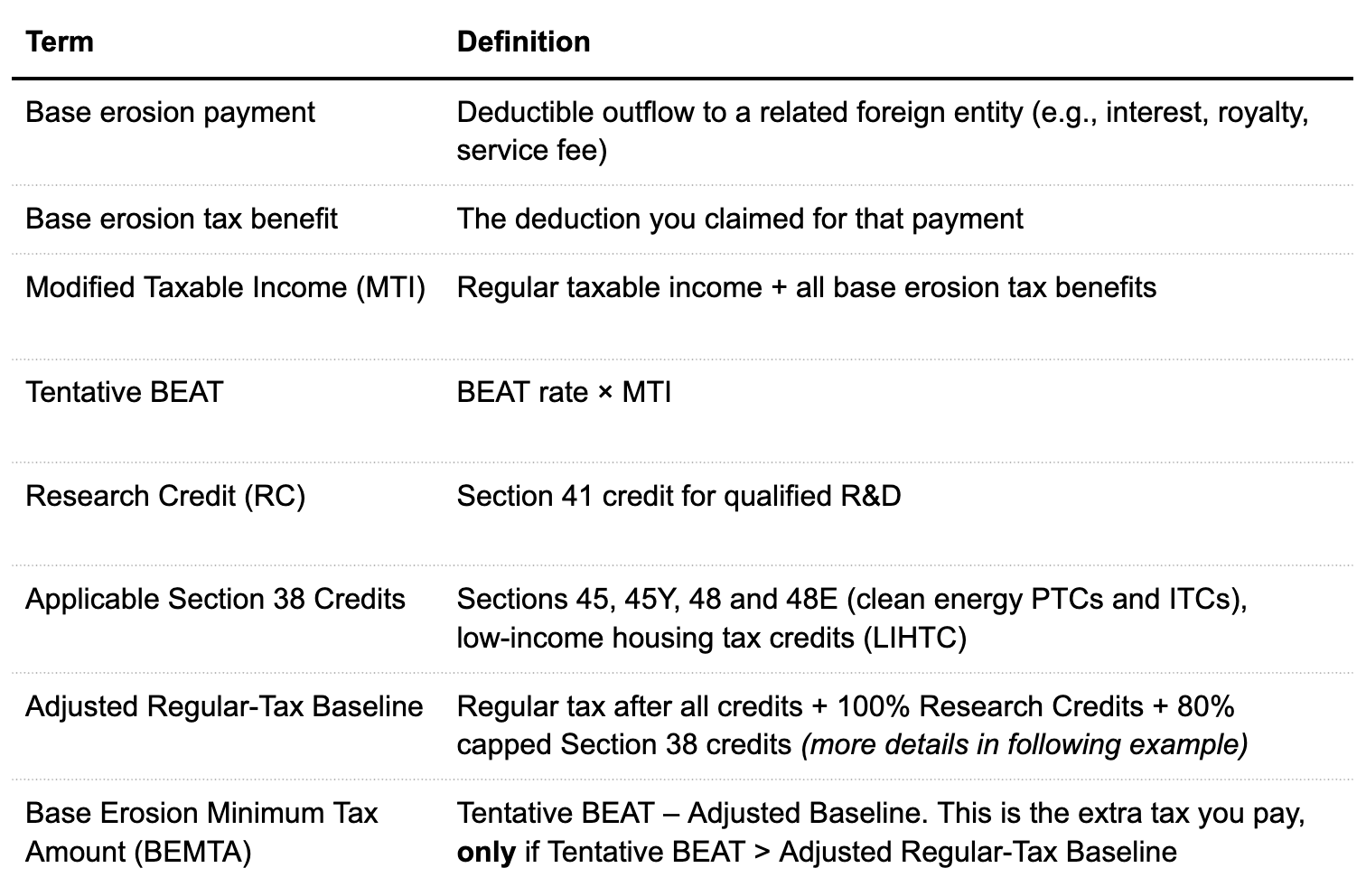

Main Components of BEAT – Every Term Explained

BEAT in Practice

What happens step-by-step? Below we will walk through a detailed example.

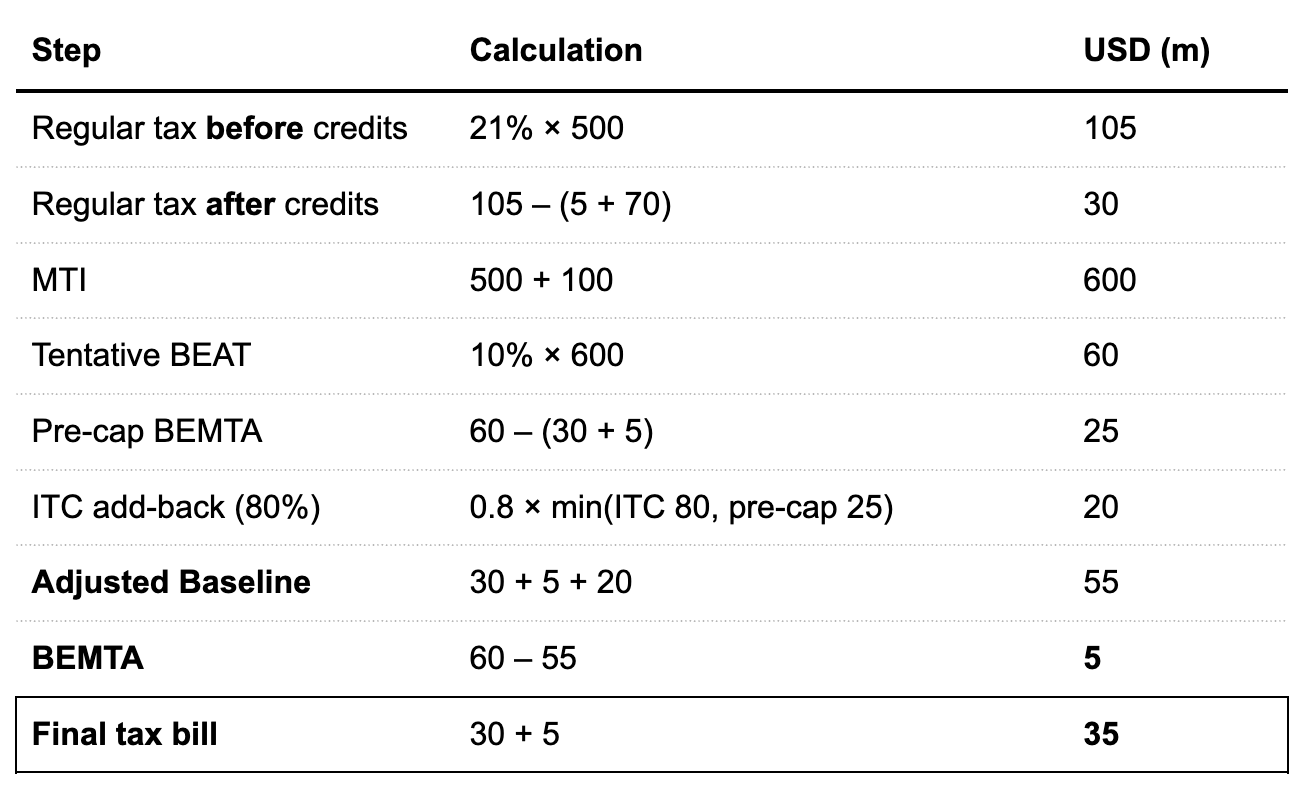

Assumptions (for Tax Year 2025):

- Taxable income = $500m

- Base-erosion deductions = $100m

- Research credit = $5m

- Energy ITC = $70m

- Corporate rate = 21% | BEAT rate = 10%

Step 1: Compute regular tax before and after credits.

Twenty‑one percent of $500m is $105m. Subtract the $5m research credit and the $70m ITC to get $30m of regular tax after credits.

Step 2: Build back the Modified Taxable Income (MTI).

Add the $100m base‑erosion deductions back to taxable income: $500m + $100m = $600m MTI. We will use MTI to calculate the Tentative BEAT figure.

Step 3: Calculate Tentative BEAT.

Apply the 10% BEAT rate to MTI: $600m × 10% = $60m.

Step 4: Find the Pre‑Cap BEMTA.

Subtract the regular tax after credits, plus the full R&D credit amount, from the Tentative BEAT figure calculated in Step 3: $60m – ($30m + $5m) = $25m. Think of this calculation as “what is the Base Erosion Minimum Tax Amount owed if R&D credits are added back to the regular tax liability?” This difference will help determine the Adjusted Baseline in Step 6.

Step 5: Restore part of the ITC under the 80% rule.

Take 80% of the lesser of (1) the total amount of applicable credits (in this case, the ITCs worth $70m), or (2) the $25m gap calculated in Step 4. The $25m gap is smaller, so: 0.8 × $25m = $20m.

Step 6: Assemble the Adjusted Baseline.

Add regular tax after credits ($30m), the research credit ($5m), and the ITC add‑back ($20m) calculated in Step 5. The resulting Adjusted Baseline is $55m. This Adjusted Baseline is used to determine whether an additional BEAT tax is owed by the firm.

Step 7: Calculate BEMTA.

Tentative BEAT of $60m minus the Adjusted Baseline of $55m equals a Base Erosion Minimum Tax Amount of $5m.This is the additional tax that the company will need to pay in addition to its regular tax.

Step 8: Determine the final U.S. tax bill.

Add BEMTA ($5m) to regular tax after credits ($30m) = $35m. This means that in total, the firm owes $35m in federal tax for 2025.

The above process is summarized in the table below:

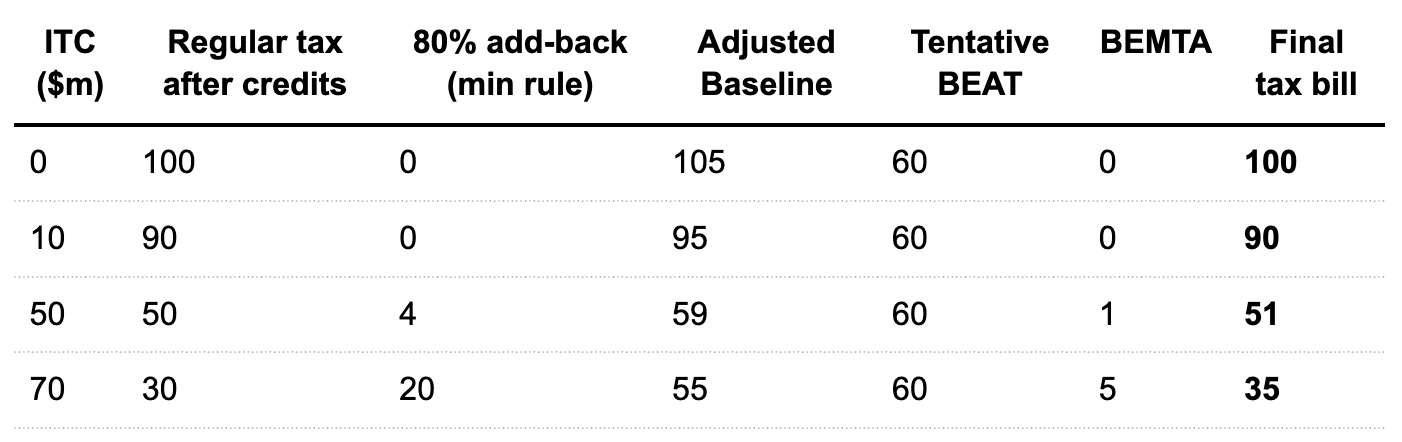

How ITCs Change the Final Tax Bill

(Same assumptions as above—only ITC varies; BEAT rate remains at 10%)

Why the rising BEMTA?

- The applicable tax credits (in this case, the ITCs) first slash the regular tax amount.

- When calculating the Adjusted Baseline for determining whether BEAT tax is owed, only 80% of the slice capped at the min(ITC, pre-cap BEMTA) goes back in.

- Once the ITC exceeds that slice, the Adjusted Baseline falls while the Tentative BEAT remains unchanged—so BEMTA goes up. As a reminder, BEMTA is the Base Erosion Minimum Tax Amount, or the difference between the Tentative BEAT and the Adjusted Baseline.

- In other words, as the Adjusted Baseline decreases and the Tentative BEAT remains the same, the BEMTA (the gap between the two) will increase.

- In the final two rows, the company’s regular tax after credits is actually below the amount it ends up paying, because BEAT steps in and raises the total. The extra BEAT charge erodes some of the benefit: although the company claims $75 million in credits, its ultimate tax bill is no lower than it would have been with just $70 million.

Note: the above example is for illustrative purposes only and holds many factors constant for purposes of showing BEMTA; energy tax credits are general business credits (GBCs) and are subject to the limitation on offset of up to 75% of total tax liability in a tax year.

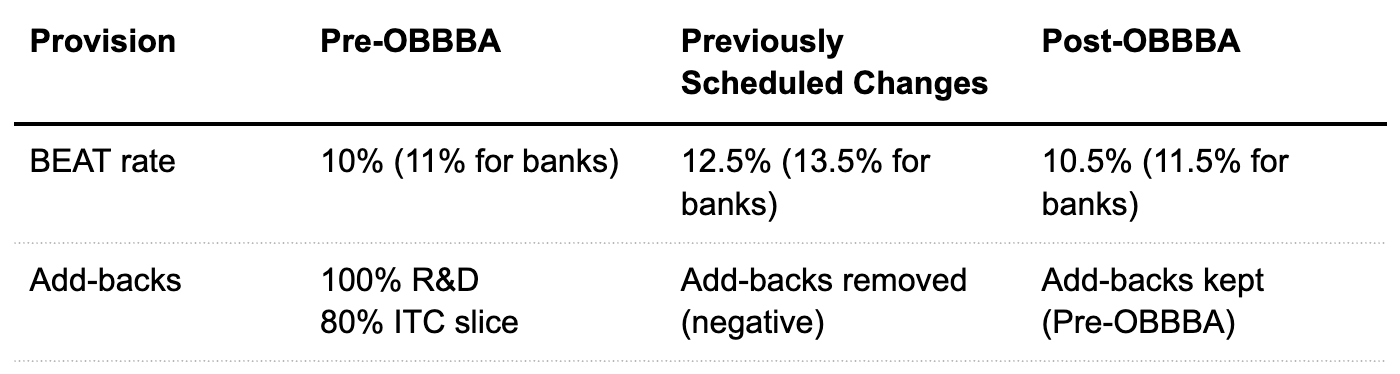

What the OBBBA Changed—and Why It Matters

The One Big Beautiful Bill Act (OBBBA), signed on July 4 2025, made three primary edits to the BEAT rules. Each one shifts the numbers you will see on tax returns for 2026 and on:

1. Permanent 10.5% BEAT rate

- Before OBBBA: 10% through 2025, then a jump to 12.5% in 2026.

- After OBBBA: the steep jump is cancelled and the rate is fixed at 10.5%.

- Note: The rate will be fixed at 11.5% for banks.

Practical effect – every $100 million of Modified Taxable Income now generates an additional $0.5 million inTentative BEAT, year-in, year-out, but it saves $2 million versus the 12.5% that was scheduled to kick-in.

2. Credit add-back mechanics unchanged

- The add-backs were scheduled to disappear after 2025, before the OBBBA came into effect. This means that all credits would have lowered the Adjusted Baseline, thus creating a harsher BEAT environment.

- 100% of the §41 research credit is still restored in the BEAT formula.

- Only 80% of the “applicable Section 38” slice is restored, and only up to the “lesser-of” cap.

Practical effect – R&D remains the best shield; large ITCs still widen the BEAT gap once they outgrow the 80% slice.

3. Applies to tax years beginning after December 31, 2025

Practical effect – calendar-year taxpayers first feel the new 10.5% rate on their 2026 return; fiscal-year filers pick it up in the first fiscal year that begins in 2026.

Why it matters for multinationals claiming clean-energy credits

- Higher floor, same cushions – Tentative BEAT rises 5%, but the 100% / 80% add-backs do not rise with it. If your 2025 model showed a razor-thin buffer, you may see a BEAT top-up in 2026.

- Predictable long-term rate – With the 12.5% step-up gone, long-term forecasts can rely on one rate, but energy-credit planning still has to respect the 80% cap.

- Credit strategy under the microscope – Front-loading a large ITC in a single year can now push you into BEAT; spreading the credit across years or boosting U.S. R&D can keep you below the threshold.

How Concentro Can Help

We work closely with our buyers to ensure they are able to maximize the benefits of their tax credit purchase and plan around BEAT appropriately. We manage the entire end-to-end process of tax credit transactions, including sourcing, diligence, and insurance.

Interested in learning more?

Book a call with us today to explore how you can leverage tax credits while navigating BEAT restrictions.