This guide covers the full lifecycle of a tax credit purchase in one place so that buyers have a single resource to refer to. There's a lot to dig into so feel free to jump to the sections most relevant to you! We also plan to keep this guide updated as the market evolves. As always, if you have questions or would like to dive deeper, we're happy to connect.

Table of Contents

- Introduction

- The Basics: What Credits Are & How We Got Here

- Market Update: The Clean Energy Credit Landscape in 2025

- How a Purchase Actually Works (and How It’s Reflected in Accounting)

- The Legal Paper: Term Sheets, TCTAs, and Tax Forms

- What Buyers Really Optimize: Risk, Price, and Timing

- Diligence: The Buyer’s Checklist

- Preparing Internally: Building Buy-Side Readiness

- Wrap-Up: Buyer Takeaways

1. Introduction

This guide is written for corporate tax and finance executives evaluating, or already active in, the transferable clean energy tax credit market. Whether you're a first-time buyer sizing up your initial transaction or a repeat participant refining your approach, the goal is the same – to provide a comprehensive, practitioner-level resource that covers the full lifecycle of a credit purchase, from market context through execution, diligence, and internal readiness.

At Concentro, we help facilitate clean energy tax credit transfers, advising corporate buyers across all deal sizes, with the majority typically falling in the $2M to $50M range. The perspectives in this guide are informed by that work – by the patterns we see across deal structures, the questions that come up in diligence, and the strategies that consistently deliver the best outcomes for buyers. Our goal is to share those learnings so that corporate tax teams, whether transacting for the first time or the tenth, can approach the market with confidence and clarity.

Much has changed in a short time. Since the first transfers closed in late 2023, legislative and regulatory developments – most notably the changes introduced by the One Big Beautiful Bill Act (OB3) – have reshaped the landscape for buyers, while transaction patterns and buyer behavior continue to shift in ways that create both complexity and opportunity.

This guide reflects where the market stands as we enter 2026, and where we see it heading.

2. The Basics: What Credits Are & How We Got Here

What Is a Transferable Credit?

Section §6418 of the Internal Revenue Code, introduced by the Inflation Reduction Act (IRA) in 2022, created a new mechanism for corporate taxpayers to reduce their federal tax liability – purchasing tax credits at a discount directly from clean energy projects.

Before this transferability framework existed, these credits were largely inaccessible to corporations, reserved for only the largest players willing to engage in complex and costly tax equity structures. Now, any company with federal tax liability can buy credits at a discount and apply them dollar-for-dollar against what they owe.

The two most common credit types in the transfer market are Investment Tax Credits (ITCs) and Production Tax Credits (PTCs). ITCs are one-time credits based on a project's eligible cost basis, typically claimed in the year the project is placed in service. PTCs are production-based credits earned over time based on a project's energy output. A third category, 45X Advanced Manufacturing Production Credits, has also gained traction as a transferable credit. Each carries a different risk profile, documentation requirement, and pricing dynamic – which we cover in detail in Section 6.2.

How the Market Developed

The market's trajectory has been remarkable. When the first transfers closed in late 2023, many corporate tax teams encountering the mechanism for the first time considered it too good to be true. Within eighteen months, that skepticism gave way to scale – industry estimates point to over $30 billion in transfers in 2024 and approximately $40 billion in 2025, with hundreds of corporate buyers now active across credit types and deal sizes.

That growth has been supported by a maturing ecosystem of intermediaries, insurers, legal advisors, and diligence infrastructure – all of which have helped standardize execution and reduce friction for new entrants.

The passage of the One Big Beautiful Bill Act (OB3) in mid-2025 introduced changes that are relevant to buyers, most notably accelerated phaseout timelines for certain credit types and tighter restrictions on projects with ties to Foreign Entities of Concern (FEOCs). We cover these developments in detail in Section 3. The core mechanics of transferability, however, remain intact – and the market's fundamentals are strong heading into 2026.

Benefits for Buyers

So why are corporate tax departments increasingly turning to transferable credits? The answer is simple – few other strategies offer a comparable combination of direct savings, manageable risk, and straightforward execution. It's a sentiment we hear often from CFOs and tax directors, and one that's worth repeating – effective tax credit transfers have the power to transform the tax department from a cost center into a profit center.

Direct cash savings & timing. Buyers typically acquire credits at 88 to 95 cents on the dollar, translating to immediate savings on every dollar of federal tax liability offset. The price primarily depends on sponsor financial strength, technology and overall market dynamics. A $20M purchase at 92 cents yields $1.6M in value, with minimal execution risk when properly structured and diligenced. What makes this even more compelling is the ability to lock in those savings almost immediately. When a credit purchase is timed just before a quarterly estimated tax payment, the benefit is realized within days rather than months. We explore timing strategies in detail in Section 6.3, but the takeaway here is straightforward – this isn't a strategy where you're waiting years to see the benefit. The value is immediate and tangible.

Favorable tax treatment. The economics are made more attractive by the IRS's treatment of these transactions. The cash paid for a credit is not deductible by the buyer, but critically, the discount received is not treated as taxable income. This means the spread between purchase price and face value flows through as pure benefit without creating an offsetting tax event.

Simplicity. For those familiar with traditional tax equity, the contrast is notable. Tax equity required corporates to access credits through partnership structures, flip mechanics, and multi-year legal arrangements. Transferability works differently, buyers purchase a credit, claim it on their return, and move on. There are no partnership interests to manage, no project-level performance risk, and no ongoing compliance burden beyond the initial transaction. The diligence and documentation requirements are manageable, and the transaction timeline is measured in weeks rather than months.

Flexibility through carryback and carryforward. Under 26 U.S.C. § 39(a)(4), unused credits can be carried back three years or forward twenty-two years. In practice, most buyers purchase exactly the amount of credit they need for a given tax year, which maximizes the time value of money. But the optionality matters, particularly for buyers whose tax positions are variable or difficult to forecast with precision. Some buyers use credits strategically to offset a large tax liability from a previous year, taking advantage of the three-year carryback window. That said, carrybacks involve specific ordering rules and timing considerations that can meaningfully affect when the benefit is realized. We cover the mechanics and practical implications of carryback strategies in Section 6.3.

Risk mitigation. The market has developed robust mechanisms to protect buyers from adverse outcomes, built around three complementary layers – thorough upfront diligence, contractual indemnities that allocate key risks back to sellers, and a mature insurance market offering comprehensive recapture coverage. When a transaction is properly structured, the risk profile is highly attractive relative to the return. We cover the risk framework in detail in Sections 5 and 6.1.

ESG alignment. In our experience, sustainability considerations tend to be a secondary factor in the investment decision rather than a primary driver. That said, some buyers do find value in the narrative – being able to point to their role in financing a portfolio of low-income community solar projects, for instance, or contributing indirectly to the broader energy transition. For companies with public sustainability commitments, it offers a way to align tax strategy with corporate values without the complexity of direct project investment.

Rules of the Road for Buyers

Transferability offers a streamlined path to tax savings, but it operates within defined boundaries. The following are the key constraints that govern how credits can be purchased and claimed by buyers.

Eligible buyer status. Only corporations and certain entities with passive activity income can purchase transferable credits. Additionally, buyers classified as Foreign Entities of Concern (FEOCs) – including specified foreign entities and foreign-influenced entities – are prohibited from receiving transferred credits. We cover the evolving FEOC landscape in more detail in Section 3.

Single transfer between unrelated parties. Once a credit is transferred, it cannot be transferred again. The buyer who acquires the credit must be the one to use it. Additionally, per IRS rules, credits can only be transferred between unrelated parties, so transfers between affiliates or commonly controlled entities are not permitted.

75% General Business Credit limitation. Like other general business credits, clean energy tax credits are subject to the limitation under Section 38, which generally caps the use of such credits at 75% of a taxpayer's net income tax liability. In practice, this means credits cannot fully eliminate your tax bill.

IRS registration requirements. Each credit must be registered with the IRS before it can be transferred, and the registration number must appear on both parties' tax returns. The buyer claims the credit on their original tax return for the year the credit is earned, alongside the IRS registration ID and a Transfer Election Statement. We cover the registration process and documentation requirements in more detail in Section 7.

Other considerations. Buyers with significant international operations should also consider how credit purchases interact with the Base Erosion and Anti-Abuse Tax (BEAT). We've addressed this topic separately in BEAT After OB3: A Practical Guide.

3. Market Update: The Clean Energy Credit Landscape in 2025

The clean energy tax credit transfer market has continued to evolve in 2025. The core mechanics of transferability remain intact but several developments this year have influenced buyer behavior, pricing, and diligence expectations. These include the passage of OB3, heightened focus on Foreign Entity of Concern (FEOC) compliance, and evolving supply-demand dynamics.

OB3: What Changed and What Stayed the Same

The One Big Beautiful Bill Act (OB3), signed on July 4, 2025, introduced broad changes to U.S. corporate taxation. While the legislation did not directly rework the statutory mechanics of clean energy tax credit transferability, it materially altered the broader tax backdrop against which credit purchases are evaluated.

Key corporate tax provisions affecting buyer demand:

- Restoration of 100% bonus depreciation, lowering taxable income for capital-intensive sectors.

- Restoration of immediate R&D expensing under Section 174, reversing amortization requirements that had increased tax liabilities in prior years.

- Enhanced Section 179 expensing, with the maximum deduction doubled to $2.5M. For mid-sized corporations in particular, this change may have a more meaningful impact on overall tax liability.

Key provisions affecting clean energy tax credits:

- Earlier phaseouts for solar and wind tax credits, though projects that “begin construction” before July 4, 2026 continue to qualify for existing incentives – meaning the market expects supply to remain strong through ~2030.

- Tighter FEOC restrictions, including provisions that may disallow credits where projects receive "material assistance" from prohibited foreign entities. An Executive Order issued shortly after OB3 directed Treasury to accelerate guidance on FEOC rules and on "beginning of construction" standards.

Net effect: OB3's most meaningful market impact has been indirect. The corporate tax provisions above collectively lowered corporate tax liabilities, reducing aggregate buyer appetite and prompting many buyers to recalibrate purchase size or exit the market for 2025 credits altogether. We discuss how this has influenced pricing and supply-demand dynamics in the sections below.

FEOC: Compliance Becoming More Central to Diligence

The FEOC provisions introduced under the Inflation Reduction Act take on greater practical importance as their phased implementation approaches in 2026. OB3 and the subsequent Executive Order sharpened attention on Prohibited foreign entities, Specified foreign entities, and Foreign-influenced entities.

Key implications for buyers

- Credits may not be transferred to specified foreign entities.

- Beginning in 2026, credits may be disallowed where projects receive “material assistance” from FEOCs, with particular relevance for equipment sourcing and manufacturing credits.

- Treasury guidance is expected to expand documentation and certification requirements, which will increasingly flow through diligence processes and contractual representations.

While FEOC restrictions have not materially constrained 2025 transaction volumes, they are already influencing how credits are underwritten and how future-year risk is priced and allocated. Buyers should expect FEOC diligence to become a standard component of transactions going forward.

(See Concentro’s FEOC: What We Know So Far and more recent Breaking: IRS Drops Interim FEOC Guidance for 48E, 45Y, and 45X for a deeper dive.)

Other Macro Factors: Supply, Demand, and Market Adjustment

Despite a year marked by legislative change and regulatory focus, the clean energy tax credit transfer market has continued to grow. Market estimates put 2025 transfer volumes at approximately $40B, representing roughly a $10B (or ~30%) increase from 2024 levels, even amid shifting buyer behavior and policy flux.

That growth, however, has not been uniform across credit types or pricing. An increase in project supply combined with reduced buyer demand in Q3 led to a broad pricing adjustment for 2025 credits. We observed:

- PTC pricing remaining relatively resilient, reflecting stronger buyer preference for production-based credits based on their lack of recapture risk and simpler qualification requirements .

- ITC pricing softening more meaningfully, with average pricing down approximately 2–3 cents compared to the same time last year, reflecting the preference for PTCs. Unfortunately, many sellers who were “holding on” to pricing expectations from the end of 2024 found themselves scrambling to find buyers in the later parts of the year.

- Credits backed by strong sponsors or parent guarantees proved more insulated from pricing pressure, though the adjustment was visible across most segments of the market.

Alongside this pricing shift, buyer behavior continued to evolve. One trend that became more pronounced in 2025 was a move away from large, single-ticket purchases toward smaller, more modular transactions. This shift, which we first noticed and highlighted in an April 2025 article titled Spotlight: The Rise of “Smaller” Tax Credit Transfers, became more pronounced following the favorable tax changes from the OB3.

The year also included a federal government shutdown, which coincided with some reported delays in the issuance of IRS pre-filing registration IDs. In practice, its impact on the tax credit transfer market was limited. While certain processes moved more slowly at times, transactions continued to close and market activity remained steady.

4. How a Purchase Actually Works (and How It’s Reflected in Accounting)

For corporate buyers, the appeal of transferable credits is not just the economics – it’s the predictability. Unlike traditional tax equity, the transfer process follows a clear, repeatable sequence, with defined documentation, timing gates, and accounting outcomes. From first look to claiming the credit, most transactions close in three to seven weeks, with several steps running in parallel.

4.1 The Purchase Process, Step by Step

The figure below illustrates a typical end-to-end timeline for a transferable credit transaction run by Concentro.

4.1.1. Confirmation of Interest

The process begins with the buyer articulating their tax credit appetite and constraints. This typically includes the target credit size, preferred credit types (e.g. ITC vs. PTC), pricing expectations, insurance requirements, and any structural or timing considerations tied to estimated tax payments.

At Concentro, this input allows us to curate a bespoke set of opportunities rather than presenting a generic list. Buyers are typically shown a range of options within their parameters – different credit types, portfolio sizes, pricing points, and risk profiles – so they can make informed trade-offs early in the process.

4.1.2. Confirmation from Seller(s)

Once the buyer indicates interest in a specific project or portfolio, Concentro seeks confirmation from the relevant seller(s) that they are willing to proceed on the proposed terms. This step ensures alignment on scope, timing, and commercial expectations before either party invests further time or cost.

In our experience, this sequencing materially improves execution certainty. By the time a transaction reaches the term sheet, both sides are aligned on economics and structure, which is why the vast majority of deals that reach this stage proceed through to closing absent diligence issues – which are uncommon given the upfront screening already performed.

4.1.3. Term Sheet

The term sheet captures agreement on the key commercial terms – credit amount, pricing, payment mechanics, indemnity framework, insurance assumptions, and timing expectations. Concentro actively facilitates this stage, helping both parties navigate market norms and, where relevant, guiding first-time buyers or sellers through the process.

Once the term sheet is executed, the transaction moves from commercial alignment to execution. At this point, deep diligence and insurance procurement begin in earnest, running in parallel with legal drafting.

4.1.4. Tax Credit Transfer Agreement (TCTA) Signed

The Tax Credit Transfer Agreement is the core legal document governing the transaction. It sets out the definitive terms of the transfer, including representations, covenants, indemnities, remedies, and closing conditions.

Concentro leverages standardized TCTA and term sheet templates that reflect current market best practices, tailoring them as needed for the specific counterparties, credit types, and project characteristics involved. This approach balances efficiency with precision, ensuring buyers receive robust protections without unnecessary friction.

4.1.5. Diligence and Insurance

Diligence and insurance underwriting typically begin shortly after the term sheet is signed and are usually completed before the execution of the TCTA.

Concentro coordinates the full diligence process, producing a structured data room and a comprehensive diligence memo for the buyer, their counsel and insurers. This work often incorporates third-party reports from established providers, for example cost segregation studies to confirm eligible basis, appraisals where fair market value is relevant, and tax opinions when required. The result is a clean, well-documented package that supports both legal review and insurance underwriting.

4.1.6. Closing and Payment

Once all conditions precedent to closing are satisfied, and IRS pre-filing registration IDs are issued, the transaction closes and funds are released in accordance with the TCTA. In some cases, delayed payment terms may have been negotiated, but we often see payment timing close to closing.

At this point, the credit is formally transferred, and the buyer is positioned to claim it on their return. While this marks the end of the transaction process, it is also where timing decisions made earlier – particularly around funding relative to estimated tax payments – translate into real economic impact. More on that in Section 6.

4.1.7. Filing and Claiming the Credit (Post-Closing)

Closing the transaction does not complete the process – the credit must be properly reported for the transfer to take effect under §6418. Both parties must attach a Transfer Election Statement to their respective tax returns, and the buyer claims the credit through Form 3800 (General Business Credit) along with the applicable credit-specific form, referencing the IRS pre-filing registration ID.

Critically, the credit must be claimed on the buyer's original tax return for the applicable tax year. If the transaction closes after April 15, the buyer must have filed for an extension – filing the original return before the transaction closes can invalidate the transfer. We cover the full documentation requirements in Section 5.4.

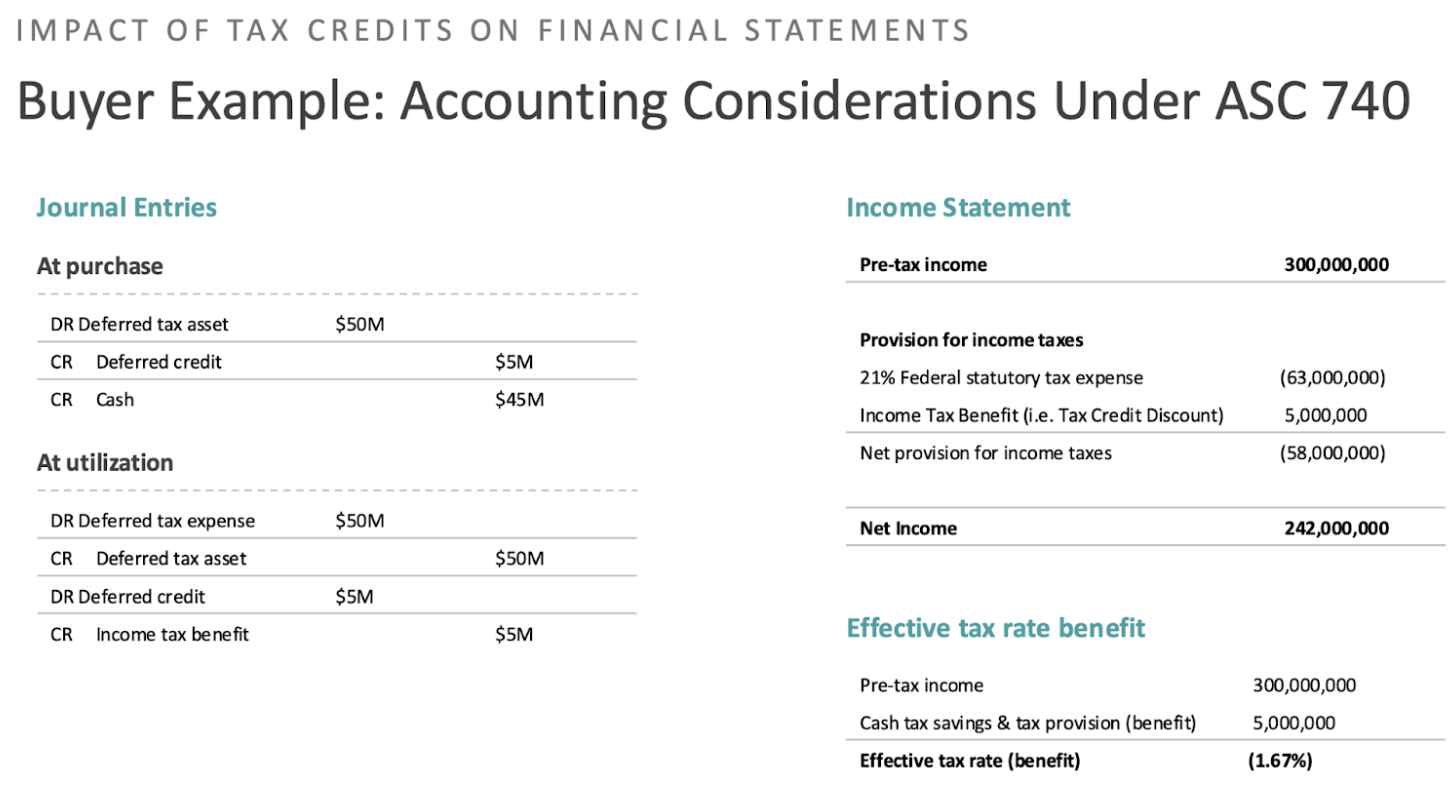

4.2 How Purchased Credits Are Reflected in Accounting (ASC 740)

From an accounting standpoint, transferable credits are generally straightforward for corporate buyers. While facts and circumstances always matter, we see most buyers account for purchased credits under ASC 740 (Income Taxes). We encourage buyers to consult with their CPA counsel to ensure that they properly account for credits in a manner consistent with their broader financial reporting systems.

The figure below illustrates a simplified same-year purchase and use example; the discussion here is intended to frame that visual rather than duplicate it.

Initial recognition. In a typical buyer fact pattern, the purchased credit is reflected within the income tax provision under ASC 740 and applied as a reduction of current federal income tax payable when claimed. Most corporate buyers size purchases for current-year utilization, so the accounting often stays within current tax rather than building meaningful carryforwards.

No taxable income on the discount. Economically, buyers pay less than the face amount of the credit, but that “discount” is not treated as taxable income to the buyer. Separately, the purchase price is not deductible for federal income tax purposes (i.e. the tax benefit is the credit itself not a deduction).

Practical takeaway. For most corporations, the accounting mirrors the commercial reality: a same-year reduction in cash taxes and income tax expense, without partnership accounting complexity – assuming the credit is purchased and utilized in the current year, as is typical in the market.

5. The Legal Paper: Term Sheets, TCTAs, and Tax Forms

While the legal documentation for transferable credit transactions is straightforward and standardized, there are several key legal documents that buyers should be aware of. For buyers, these documents serve three core functions: (i) align economics, (ii) allocate risk, and (iii) satisfy IRS requirements. This section provides a high-level tour of each and what buyers should focus on.

5.1 The Term Sheet

Purpose. The term sheet is a non-binding document that captures commercial alignment before parties incur the time and cost of full diligence and legal drafting. With limited exceptions (e.g., confidentiality and exclusivity), it does not create a legal obligation to close.

Key elements buyers should expect include the following (non-exhaustive):

- Credit profile: credit type, tax year, estimated amount, and placed-in-service assumptions.

- Price and payment mechanics: price per dollar of credit, buyer legal cost reimbursement, and funding window. These are generally the key commercial terms to align at the term sheet stage, with more nuanced legal provisions negotiated in the Tax Credit Transfer Agreement (TCTA).

- Structural assumptions: eligibility for bonus adders (e.g. PWA, energy community), registration and election timing.

- Risk framework: high-level indemnity and insurance expectations. In some cases, the principal representations and covenants are also aligned at this stage, though this is less common.

- Conditions precedent to closing: it is common to agree on the key conditions and documentation required for closing before the diligence process begins.

- Process controls: exclusivity period, tax contest process control, and change-in-tax-law provisions.

Why it matters. A well-structured term sheet minimizes renegotiation later and creates execution certainty. In our experience, once a term sheet is signed, transactions typically proceed to closing unless diligence surfaces an issue. Even then, those issues are often remediable rather than deal-breaking – for example, identifying a missing third-party report and working with the developer to have it completed.

5.2 The Tax Credit Transfer Agreement (TCTA)

Purpose. The Tax Credit Transfer Agreement is the definitive, binding contract that effects the transfer of credits under IRC §6418 and makes the commercial terms legally enforceable. This is the document where buyer protections are established and upheld.

Core TCTA sections buyers should understand (non-exhaustive):

- Sale mechanics: credit amount, price, cash payment requirement, and closing timing.

- Representations: key representations made by the seller to confirm eligibility and the absence of structural issues that could trigger a disallowance – including project eligibility, placed-in-service status, credit rate, basis, compliance with applicable tax rules, and absence of prior transfers, among others.

- Covenants: forward-looking obligations for the seller to ensure ongoing qualification and avoid potential recapture events, including credit registration, transfer elections, recordkeeping, maintenance of insurance, commercially reasonable operation of the system, and cooperation with audits.

- Indemnities: protection against disallowance, recapture, or other loss of credits, typically on an after-tax basis. In effect, the indemnities transfer risk back to the seller in the event of a breach that results in a loss to the buyer.

- Audit and defense provisions: control of IRS examinations and coordination between buyer and seller.

- Termination rights: including failure of conditions precedent and certain adverse changes in tax law.

Why it matters. The TCTA is the legally binding document that defines the commercial terms, establishes the seller's legal representations around qualification, and provides the buyer's downside protections in the event something goes wrong. As such, it is critical that buyers engage experienced counsel to ensure the TCTA is airtight and tailored to their specific needs.

5.3 Tax Credit Insurance (if applicable)

Purpose. Tax credit insurance provides an additional layer of protection beyond contractual indemnities. Where the developer or seller is a strong counterparty with a robust balance sheet, many buyers are comfortable relying solely on indemnities – sometimes paired with a parent guarantee. In other cases, buyers elect to add insurance to further de-risk the transaction and enhance the credit of the counterparty. We discuss how insurance fits into the broader risk framework, and when buyers typically elect to use it, in Section 6.1.

What a typical policy covers:

Coverage depends heavily on the terms procured, but the most common approach is for buyers to request "full-wrap" coverage, which covers all risks not stemming from fraud, misrepresentations, or forward-looking willful actions. Typically, coverage is framed around four core buckets:

- Qualification: does the property qualify for the credit elected? This may include general qualification, bonus adder qualification, and related eligibility requirements.

- Structure: is the financial and corporate structuring sound, and will it be respected for tax purposes? This includes step-up transactions and overall taxpayer qualification – i.e. confirming that the seller is the correct entity within the corporate structure to claim and transfer the credit.

- Basis: has the basis used to calculate the credit been properly determined, and is the full basis eligible? This ensures the credit amount is correct and does not include ineligible items (e.g. roofing costs for a solar installation).

- Recapture: is there any future event that could trigger recapture by the IRS? In essence, this covers risks that may prevent the project from continuing operations or maintaining the same ownership during the five-year recapture period.

Coverage is generally procured at 100% of the face value of the credit, though in some cases buyers request limits in excess of 100%. The policy limit represents the maximum amount covered, but coverage typically includes the loss itself plus associated interest, penalties, and legal costs.

Material exclusions buyers should understand. While policies vary by carrier and underwriter, the most consequential exclusions tend to center on post-closing, intentional actions rather than technical or diligence-related issues. Common material exclusions include:

- Willful disposition or transfer of the underlying asset during the recapture period (e.g., a voluntary sale or prohibited ownership change by the project owner).

- Fraud or intentional misconduct by the insured or insured-affiliated parties.

- Known violations or deliberate non-compliance that occur after policy binding.

- Certain change-in-law risks, depending on policy structure and negotiation – this is a key item to negotiate in the policy.

Beyond standard exclusions, buyers and their counsel should review whether any additional exclusions could limit coverage around a key project risk. It is also worth noting that non-standard exclusions can signal heightened risk perception by the underwriter, which may itself be informative when evaluating the transaction.

Why it matters. Insurance provides peace of mind for tax directors who want to ensure every box is checked from a risk coverage perspective, but it also serves as independent validation – an expert third party evaluating the project risks and putting its own balance sheet behind them. Notably, tax credit insurers currently operate under near-zero loss mandates, meaning the underwriting bar is high and a policy that clears it provides strong additional confidence in the transaction.

5.4 IRS Forms and Filings

Purpose. Even a perfectly drafted contract does not, by itself, transfer a tax credit. The IRS filings are what make the transfer effective for tax purposes.

Key items buyers should be aware of:

- IRS pre-filing registration and issuance of a registration ID for the eligible credit property

- Transfer election statement, filed with both parties’ returns

- Form 3800 (General Business Credit), through which the credit is ultimately claimed

- Credit-specific forms (e.g. Form 3468 for ITCs or the applicable PTC form)

Why it matters. Timing and accuracy are critical. Without proper registration and a valid transfer election, the credit cannot be claimed – even if cash has changed hands.

6. What Buyers Really Optimize: Risk, Price, and Timing

At a high level, buying transferable tax credits can look like a pricing exercise: find a credit at a discount and apply it against your tax bill. In practice, that framing misses how experienced buyers actually approach the market.

Sophisticated tax teams optimize across three variables simultaneously: risk, price, and timing. Price matters, but it is rarely the primary decision driver. Risk determines whether a transaction clears internal approvals at all, and timing often determines how much value is ultimately realized. Understanding how these variables interact is what separates one-off purchases from repeatable, programmatic strategies.

We start with risk, because everything else flows from it.

6.1 Risk: What Actually Matters (and How Buyers Mitigate It)

For first-time buyers, the word “risk” can sound ominous – especially when diligence, indemnities, and insurance enter the conversation. In reality, the risk of recapture in properly structured transactions is generally low, and most transfers are best understood as highly documentable tax attributes, not speculative investments.

The market’s emphasis on diligence, contracts, and insurance (where appropriate) is not driven by an expectation of problems. It reflects how the transfer market has matured to meet the approval standards of naturally risk-averse, public-company tax departments. Understanding how these protections fit together simply allows buyers to evaluate opportunities with confidence.

A useful way to think about risk in these deals is to separate it into two buckets:

- Backward-looking risk: Is the credit valid as generated – properly calculated, supported by documentation, and eligible under the rules?

- Forward-looking risk: After transfer, could a post-closing event jeopardize the buyer’s benefit (for example, by triggering recapture)?

The risk framework is designed to address both.

The Three Pillars of Risk Mitigation

In practice, risk management rests on three complementary pillars, each addressing a different aspect of the risk profile.

1. Diligence: table stakes

Diligence is non-negotiable for experienced buyers. When done properly, it addresses the vast majority of backward-looking risk. This is where most uncertainty is eliminated, ensuring the buyer is acquiring a properly calculated, well-documented credit rather than underwriting ambiguity.

2. Contractual protections

The Tax Credit Transfer Agreement converts diligence conclusions into enforceable protections.

- Indemnities allocate backward-looking risk to the seller if a credit is later reduced or disallowed.

- Covenants address forward-looking risk by restricting post-closing actions that could jeopardize the credit.

- Parent guarantees or other credit support are sometimes added where the seller is a project-level entity.

3. Insurance (where used)

In our experience, the majority of transactions include insurance, with many buyers willing to accept a slightly lower discount in exchange for internal comfort. Others may prefer to rely on a parent guarantee and/or contractual protections in order to optimize price.

While insurance is often described as the "third" layer, in practice it functions as the first line of defense. If a covered loss occurs, the insurer pays out first, with indemnities only coming into play if losses exceed policy limits or fall outside coverage. This structure reduces enforcement risk and avoids the need for buyers to pursue recovery directly from the seller.

Counterparty strength is often a key factor here. When the seller is a large, reputable developer with a strong balance sheet, buyers may get comfortable relying simply on the contractual protections and a parent guarantee (where appropriate). In other cases – e.g. larger purchases, portfolio transactions, or newer developers – insurance from a third party provides an efficient way to further de-risk the transaction.

6.2 Pricing: What Drives the Discount

Pricing in the transferable tax credit market is not monolithic. Discounts vary meaningfully depending on credit type, deal structure, and seller profile – and understanding these drivers is essential for buyers looking to benchmark opportunities, identify value, and avoid overpaying for perceived safety.

Pricing by Credit Type

The table below summarizes typical pricing ranges observed in late 2025 and early 2026, alongside key structural attributes that influence both risk profile and market pricing.

How to read this table:

Structure distinguishes between one-time ITCs (claimed in the year a project is placed in service) and production-based PTCs (claimed over multiple years of output or as a single "spot" year). This distinction drives several downstream differences, including recapture exposure and documentation requirements.

Typical projects per deal reflects how credits are commonly packaged. Utility-scale transactions typically involve a single large project, while distributed-generation credits are routinely bundled, with residential aggregators often packaging hundreds of systems into a single transaction.

Recapture risk refers to the ITC vesting schedule under Section 50. ITCs vest at 20% per year over five years; if the underlying asset is disposed of or ceases to qualify during this period, the unvested portion must be repaid. PTCs are not subject to recapture.

Prevailing Wage & Apprenticeship (PWA) compliance, is required for projects larger than 1MW to receive the full credit rate. Compliance must be maintained through the five-year recapture period (ITC) or ten-year credit period (PTC).

OB3 policy outlook: Solar and wind credits face an accelerated phaseout – projects must begin construction before July 4, 2026, or be placed in service by December 31, 2027. Storage and other non-solar/wind technologies retain full credit availability through 2033. 45X manufacturing credits are available in full through 2029 before phasing down.

2025-2026 pricing context:

As discussed in Section 3, OB3's corporate tax changes reduced aggregate buyer demand in 2025, leading to a broad pricing adjustment, particularly for ITC credits, which softened approximately 3-5 cents from late 2024 levels. PTC and 45X pricing proved more resilient, reflecting the absence of recapture risk and stronger buyer familiarity, though both softened modestly to the low-90s.

As 2026 begins, market activity is picking up. Many buyers who paused in 2025 are expected to re-enter with greater clarity on their tax positions – a pattern similar to what followed the 2017 Tax Cuts and Jobs Act. For buyers, the current environment presents an opportunity: pricing remains at historically attractive levels, competition is lower than in prior years, and supply across credit types is robust.

Beyond Credit Type: Other Factors That Influence Pricing

Within any given credit category, pricing can vary by several cents depending on counterparty, deal structure, and documentation complexity.

Counterparty quality. The creditworthiness of the seller is one of the most significant pricing drivers. Investment-grade sponsors or those offering parent guarantees can command premiums of 3-5 cents above comparable credits from smaller developers. Buyers willing to transact with newer sponsors can capture pricing upside but should ensure robust insurance coverage is in place.

Deal size and structure. Larger single-project transactions (typically $20M+) tend to price 2-3 cents higher than smaller deals, reflecting transaction cost efficiency and the correlation between deal size and sponsor quality. Smaller credits offer distinct advantages – faster execution, flexibility for "top-up" purchases, and lower barriers for first-time buyers. We explored this dynamic in a 2025 article, Spotlight: The Rise of "Smaller" Tax Credit Transfers.

Diligence and documentation. Not all credits require the same underwriting effort. Utility-scale ITCs typically involve more extensive review – complex financing structures, full PWA documentation, and detailed cost segregation studies. Distributed-generation and 45X credits tend to be more straightforward. FEOC material assistance rules, effective January 1, 2026, have added complexity for projects beginning construction after that date.

Bonus adders. Credits claiming domestic content, energy community, or low-income adders carry higher face values but require additional documentation. Credits with validated adders may price at par or a slight premium; those without robust support may face insurer scrutiny and pricing pressure.

Pricing is a function of credit type, counterparty quality, and deal structure. The current market offers buyers an unusual combination of attractive pricing, robust supply, and reduced competition – an environment where those who act with clarity can capture meaningful value.

6.3 How Timing Works

Timing is one of the most underappreciated drivers of value in tax credit transactions. Buyers who focus exclusively on price often leave significant savings on the table – because exactly when you contract, fund, and utilize a credit can matter as much as the discount itself.

We covered this topic in depth in our June 2025 article, Tax Credit Timing: How Buyers Should Think About When to Purchase Tax Credits. This section summarizes the key concepts and their practical implications for buyers.

The Three Dates That Matter

Understanding how timing works requires distinguishing between four separate dates – each of which can be optimized independently:

The interplay between these dates is where the real opportunity lies. Because the savings on a credit purchase are realized over days or weeks rather than over twelve months, the effective annualized yield on a well-timed transaction can be significantly larger than the nominal discount paid. Buyers who commit early and align funding with their estimated tax schedule are best positioned to capture this.

Two Strategies Worth Understanding

"Pay now, save now." This is the most common approach – fund a credit purchase shortly before a quarterly estimated tax payment is due. Instead of remitting cash to the IRS, the buyer pays the seller at a discount and applies the credit against the liability. The benefit is realized within days.

Example: A buyer closes on a $5M credit at 90 cents two weeks before their Q3 estimated payment. They pay $4.5M to the seller instead of $5M to the IRS – $500,000 in savings captured in a 14-day window.

"Commit now, pay later." In some cases, sellers agree to delayed funding windows, allowing buyers to utilize credits against estimated taxes before cash changes hands. This effectively allows the buyer to reduce their tax payments immediately while deferring the purchase price outlay – a powerful liquidity tool.

Example: A buyer executes a TCTA in March for a project placed in service in May. They apply the credit against their Q2 estimated payment (due June 15) but don't fund the purchase until August. The result is an immediate tax relief with delayed cash outflow.

Avoiding Year-End Congestion

Many buyers default to purchasing credits late in the year, closer to year-end or their extended filing deadline. This approach has clear drawbacks:

- Pricing pressure. Demand has historically spiked in late Q4 as buyers rush to deploy remaining tax appetite, compressing discounts and reducing leverage. While the second half of 2025 was softer than prior years, the structural incentive for year-end crowding remains – particularly as buyer appetite normalizes in 2026.

- Liquidity inefficiency. By late Q4, most corporations have already paid their estimated taxes for the year. Purchasing credits at this stage requires an upfront cash outlay followed by a refund claim – a process that can take months to resolve.

- Execution risk. IRS pre-filing registration turnaround times can extend during peak periods, and projects with late-Q4 expected placed-in-service dates carry the risk of construction delays pushing PIS into the following calendar year, shifting the credit's applicable tax year entirely. Experienced buyers mitigate this through tiered pricing or right-of-first-refusal (ROFR) provisions for slipped credits.

Illustrative Comparison: September-Funded vs. Following-Year April-Funded Credit

The table below illustrates how timing affects the realization of benefit – even for the same credit at the same price.

The nominal discount may be identical in both scenarios. But the September buyer captures the benefit almost immediately, while the April buyer has effectively paid twice – once to the IRS in estimated payments throughout the year, and again to the seller at filing – before eventually recovering their savings through a refund that may not arrive until mid-to-late 2026.

For buyers navigating more complex timing scenarios – including purchases made after year-end, carryback strategies, and IRS refund mechanics like Form 4466 – see Understanding timelines: A guide to purchase, carry-back and refund timings for tax credit buyers.

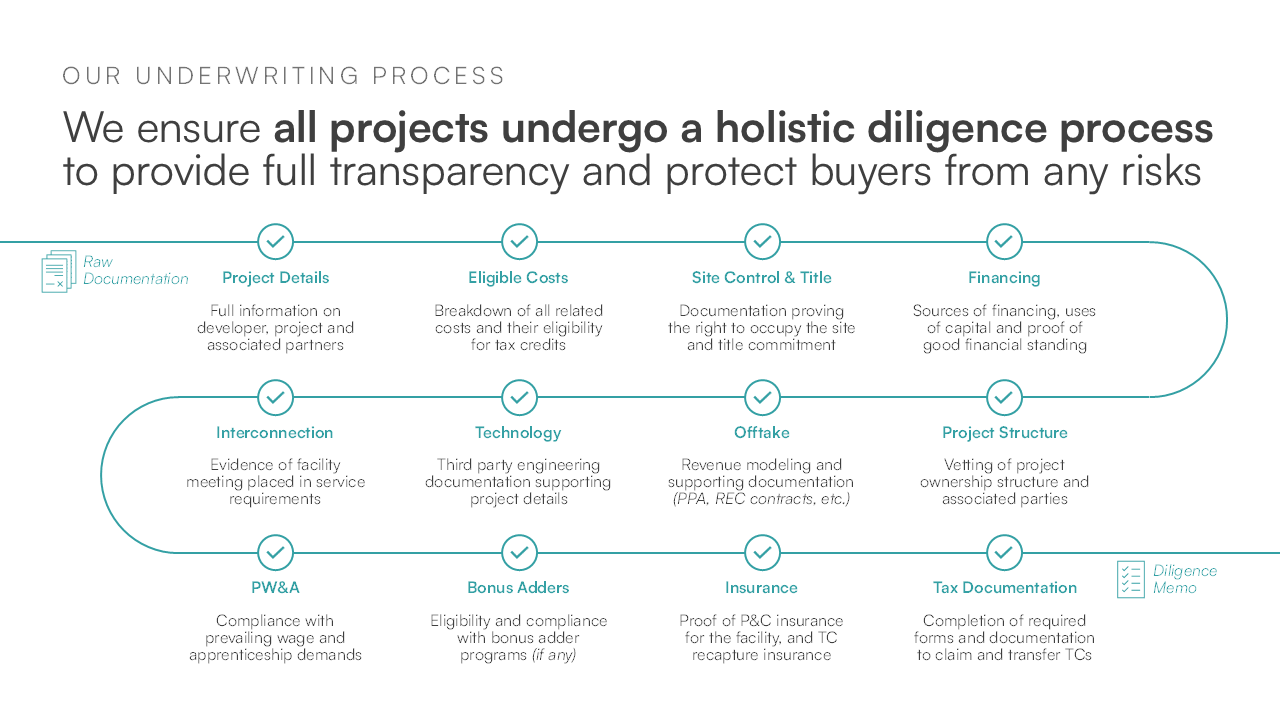

7. Diligence: The Buyer’s Checklist

Section 6.1 established that diligence is the foundation of the risk framework – the first line of defense that eliminates the vast majority of backward-looking risk before a transaction closes. This section translates that principle into practice, providing buyers with a clear view of what a comprehensive diligence process looks like and what they should expect from a well-structured transaction.

What Diligence Covers

The graphic below illustrates the key diligence categories that Concentro evaluates for every transaction. Each project moves through a structured review process – from raw documentation to a comprehensive diligence memo that supports buyer counsel review, insurance underwriting, and internal approvals.

The categories shown reflect the core areas of inquiry. The table below proides additional detail on what each involves, why it matters, and whether it applies to all transactions or only in specific circumstances.

Concentro’s Role

Concentro coordinates the end-to-end diligence process for every transaction we facilitate. This includes preparing a structured data room, conducting independent review across each category, and producing a comprehensive diligence memo for buyer counsel and insurers.

The goal is to deliver a clean package – one that supports internal approvals, legal review, and insurance procurement without requiring buyers to build diligence infrastructure in-house. For buyers transacting for the first time, this can meaningfully reduce execution risk and internal resource burden. For repeat buyers, it ensures consistency and efficiency across transactions.

The bottom line: diligence is not a formality, it is the mechanism by which risk is identified, documented, and allocated before closing. Buyers should expect a structured, comprehensive process and should be cautious of any transaction where diligence feels rushed, incomplete, or opaque.

8. Preparing Internally: Building Buy-Side Readiness

Internal alignment is a prerequisite for efficient execution. Buyers who enter the market without clarity on their parameters, approval processes, and risk framework encounter avoidable friction – and in a market where timing drives value (Section 6.3), avoidable friction is avoidable cost. This section outlines the key decisions to work through before engaging with sellers or intermediaries.

Establish Internal Parameters

Credit appetite and parameters. Define your target size range based on projected federal tax liability, keeping in mind the 75% General Business Credit (GBC) limitation. Determine which credit types fit your diligence capacity and internal preferences – whether you favor ITCs, PTCs, or are open to both. Consider whether you're comfortable with portfolios of smaller bundled credits or prefer single-project transactions.

Approval authority. Clarify who can approve transactions at various sizes and what documentation is required. Where possible, seek approval for a defined set of parameters (e.g. credit type, size range, counterparty quality, pricing floor) rather than requiring fresh review for each individual deal. This preserves flexibility without sacrificing governance and allows your team to move quickly when the right opportunity surfaces.

Risk framework and structuring. Decide how you want transactions structured from a risk perspective. Will you require insurance on all deals, or are contractual indemnities and parent guarantees sufficient for strong counterparties? For non-investment-grade sellers, what combination of insurance and indemnity support is acceptable? Having a clear position here before you engage the market avoids delays at the term sheet stage.

Timing windows. Identify when your quarterly estimated tax payments fall and how that aligns with your preferred funding windows. As discussed in Section 6.3, aligning credit purchases with your estimated tax schedule can significantly enhance effective returns. Buyers who map this out in advance can act decisively when opportunities arise rather than scrambling to align internal approvals with external deadlines.

Addressing Common Internal Questions

For many corporate buyers, particularly those transacting for the first time, the decision to purchase tax credits requires buy-in from stakeholders beyond the tax department. CFOs, general counsel, and in some cases audit committees will have questions. In our experience, the most common concerns are predictable and addressable:

"What happens if the credit is disallowed or recaptured?" This is typically the first question from legal or risk teams. The answer lies in the layered protection structure covered in Section 6.1 – diligence eliminates most backward-looking risk, contractual indemnities allocate residual risk to the seller, and insurance (where used) provides a direct payout mechanism that avoids the need to pursue recovery from the counterparty. For a properly structured transaction, the buyer's downside is well-defined and well-mitigated.

"Is this an established market or are we early?" The market has processed over $30 billion in transfers in 2024 alone, with 2025 volumes estimated at approximately $40 billion. Transaction documentation is increasingly standardized, a mature insurance market provides third-party validation of risk, and hundreds of corporate buyers – including many Fortune 500 companies – have transacted. This is no longer a nascent space.

"How much internal resource does this require?" When working with an experienced intermediary, the internal burden is manageable. The intermediary coordinates diligence, documentation, and insurance. Buyer-side involvement is concentrated around defining parameters, reviewing the TCTA with counsel, and coordinating IRS filings – a workload measured in hours, not weeks.

For First-Time Buyers

- Start with a pilot transaction. A smaller initial purchase builds internal familiarity with diligence, documentation, and IRS filings before committing to larger volumes. It also gives stakeholders a concrete reference point for evaluating whether to expand the program in subsequent years.

- Engage experienced counsel. External tax counsel with transfer market experience can accelerate TCTA review and provide comfort to internal stakeholders. Concentro has worked with over 10 law firms on buyer-side transactions and is happy to provide recommendations.

- Leverage intermediary infrastructure. For teams without dedicated resources, an experienced intermediary can meaningfully reduce execution burden by coordinating diligence, documentation, and insurance procurement. When evaluating an intermediary, buyers should consider:

- depth of diligence process and documentation standards,

- breadth of seller relationships across credit types and deal sizes,

- track record with insurance carriers and buyer-side counsel, and

- willingness to serve as a hands-on execution partner rather than simply matching buyer to seller.

- Build toward a repeatable program. The most sophisticated buyers we work with treat their first transaction as the foundation for a programmatic strategy. They document their internal process, capture lessons learned, and establish pre-approved frameworks that allow them to transact more efficiently in subsequent years. The difference between a one-off purchase and a repeatable program is not scale – it's preparation.

9. Wrap-Up: Buyer Takeaways

This guide has covered a lot of ground, from the mechanics of transferability and the current market landscape, through pricing, timing, risk, diligence, and internal readiness. The table below distills the key principles that, in our experience, separate buyers who extract maximum value from those who leave money on the table.

Looking Ahead

The transferable credit market enters 2026 in a compelling position for buyers. OB3's accelerated phaseout timelines are driving a wave of project development activity as developers race to meet "begin construction" deadlines, which means robust supply across credit types through at least the end of the decade. At the same time, the pricing reset that followed OB3's corporate tax changes has created an environment where discounts remain at historically attractive levels, particularly for ITC credits, while competition among buyers is lower than at any point since the market's inception.

For companies that have been evaluating the market from the sidelines, the conditions are unlikely to be more favorable. Supply is deep, pricing is attractive, and the infrastructure around diligence, insurance, and legal documentation has matured to a point where execution is well understood and straightforward. For those already active, the opportunity is to deepen and systematize – expanding across credit types, optimizing timing strategies, and building the internal muscle to transact efficiently at scale.

The tax credit transfer market has moved from experiment to established practice in just over two years. The companies that engage now – with clarity on their parameters, the right structure, and the right partners – are best positioned to capture value as the market continues to evolve.

Concentro publishes regular market updates, pricing insights, and policy analysis for corporate buyers. Subscribe to our newsletter to stay across the latest developments – or get in touch if you're ready to explore how tax credits fit into your tax strategy.